Page 21 - 60

P. 21

population grows and increases in affluence and

economic activity, as well as by other end-uses,

such as petrochemicals.

Increased power production from renewable

sources, which include – although to a lesser extent

- hydro and nuclear (the latter mostly in China but

also in other countries), will be one of the dominant

themes over the next decades. While decarboniza-

tion policies and several societal trends are some

of the key drivers behind this surge, an important

foundation is the huge improvement in economics

of power produced from wind, offshore and onsho-

re, and from photovoltaic plants (figure 7). Where-

as power production from wind has been broadly

competitive with that from fossil fuel sources on

purely economic grounds for some time, the pho-

tovoltaic energy is rapidly closing the gap. Therefo-

re, in a few years there will be no longer a need for

subsidies or incentives, and PV will be able to com-

pete on purely economic grounds. The share of

power production from renewables, therefore, will

grow rapidly almost everywhere (figure 8). The EU

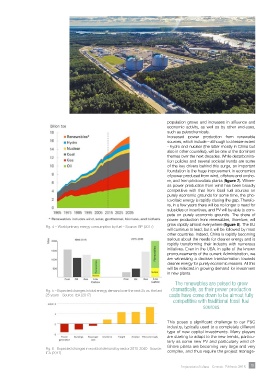

Fig. 4 – World primary energy consumption by fuel – Source: BP (2017)

will continue to lead, but it will be followed by most

other countries. Indeed, China is rapidly becoming

serious about the needs for cleaner energy and is

rapidly transforming their industry with numerous

initiatives. Even in the USA, in spite of the known

pronouncements of the current Administration, we

are witnessing a decisive transformation towards

cleaner energy for purely economic reasons. All this

will be reflected in growing demand for investment

in new plants.

The renewables are poised to grow

Fig. 5 – Expected changes in total energy demand over the next 25 vs. the last dramatically, as their power production

25 years – Source: IEA (2017) costs have come down to be almost fully

competitive with traditional fossil fuel

sources

This poses a significant challenge to our E&C

industry, typically used to a completely different

type of new capital investments. Many players

are starting to adapt to the new trends, particu-

larly as some new PV and particularly wind of-

fshore plants are becoming very large and very

Fig. 6 – Expected changes in world oil demand by sector 2015-2040 - Source: complex, and thus require the project manage-

IEA (2017)

Impiantistica Italiana - Gennaio- Febbraio 2018 19