Page 24 - 60

P. 24

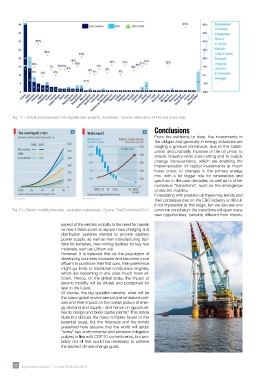

Fig. 12 – Actual and proposed LNG regasification projects, worldwide – Source: elaboration of IHS and Snam data

Conclusions

From the evidence to date, the investments in

the oil&gas and generally in energy industries are

staging a gradual comeback, due to the stabili-

zation and probably increase of the oil price; to

drastic industry-wide cost-cutting and to supply

change improvements, which are enabling the

implementation of capital investments at much

lower costs; to changes in the primary energy

mix, with a far bigger role for renewables and

gas than in the past decades; as well as to other

numerous “transitions”, such as the emergence

of electric mobility.

Forecasting with precision all these may trends and

their consequences on the E&C industry is difficult

if not impossible at this stage, but we can see one

Fig. 13 – Electric mobility forecasts – probably understated – Source: The Economist (2017) common conclusion: the transitions will open many

new opportunities, certainly different from historic

aspect of the electric mobility is the need for massi-

ve new infrastructure to support new charging and

distribution systems needed to provide capillary

power supply, as well as new manufacturing faci-

lities for batteries, new mining facilities for key raw

materials, such as Lithium etc.

However, it is believed that as the population of

developing countries increases and becomes more

affluent to purchase their first cars, their preference

might go firstly to traditional combustion engines,

which are becoming in any case much more ef-

ficient. Hence, on the global scale, the impact of

electric mobility will be diluted and postponed for

later in the future.

Of course, the big question remains: what will be

the future global environmental and emissions poli-

cies and their impact on the overall picture of ener-

gy demand and supply - and hence on opportuni-

ties to design and build capital plants? This article

does not discuss the many complex facets of this

essential issue, but the forecasts and the trends

presented here assume that the world will adopt

“some” key environmental and emission mitigation

policies in line with COP 21 commitments, but pro-

bably not all that would be necessary to achieve

the desired climate change goals.

22 Impiantistica Italiana - Gennaio- Febbraio 2018