Page 32 - 60

P. 32

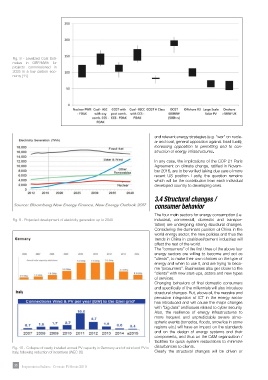

Fig. 8 - Levelized Cost Esti-

mates in GBP/MWh for

projects commissioned in

2025 in a low carbon eco-

nomy [11]

and relevant energy strategies (e.g. ”war” on nucle-

ar and coal, general opposition against fossil fuels);

increasing opposition to permitting and to con-

struction of energy infrastructures.

In any case, the implications of the COP 21 Paris

Agreement on climate change, ratified in Novem-

ber 2016, are to be verified taking due care of more

recent US position. Lastly, the question remains

which will be the contribution from each individual

developed country to developing ones.

3.4 Structural changes /

consumer behavior

The four main sectors for energy consumption (i.e.

Fig. 9 - Projected development of electricity generation up to 2040 industrial, commercial, domestic and transpor-

tation) are undergoing strong structural changes.

Considering the dominant position of China in the

world energy sector, the new policies and thus the

trends in China in coal/steel/cement industries will

affect the rest of the world.

The “consumers” of the first three of the above four

energy sectors are willing to become and act as

“clients”, to make their own choices on the type of

energy and when to use it, and are trying to beco-

me “prosumers”. Businesses also get closer to the

“clients” with new start-ups, actors and new types

of services.

Changing behaviors of final domestic consumers

and specifically of the millennials will also introduce

structural changes. But, above all, the massive and

pervasive integration of ICT in the energy sector

has introduced and will cause the major changes

with “big data” and issues related to cyber security.

Also, the resilience of energy infrastructures to

more frequent and unpredictable severe atmo-

spheric events (tornados, floods, snow/ice in some

regions etc.) will have an impact on the standards

and on the design of energy systems and their

components, and thus on the O&M organization /

facilities for quick system restorations to minimize

Fig. 10 - Collapse of newly installed annual PV capacity in Germany and of wind and PV in disturbances to clients.

Italy, following reduction of incentives (WEC [1]) Clearly the structural changes will be driven or

30 Impiantistica Italiana - Gennaio- Febbraio 2018