Page 33 - 60

P. 33

response, intelligent homes, smart grids;

• interconnections between countries.

IEA underlines that “overall, the grid is modernizing

and moving away from a pure electricity delivery bu-

siness to an integrated platform for data and servi-

ces, enabled by rapid progress in digital information

and communications technologies, which grew to

over 10% of networks spending”. This is changing

the roles of all the stakeholders completely.

4. Summary and conclusions

There will be no shortage of fossil fuels for very

many decades; there will be however socio-poli-

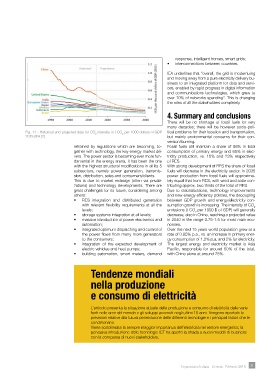

Fig. 11 - Historical and projected data for CO intensity in t CO per 1000 dollars of GDP tical problems for their location and transportation,

2

2

2015 (IEA [2] but mainly environmental concerns for their con-

version/burning.

refrained by regulations which are becoming, to- Fossil fuels still maintain a share of 86% in total

gether with technology, the key energy market dri- consumption of primary energy and 65% in elec-

vers. The power sector is becoming ever more fun- tricity production, vs. 10% and 23% respectively

damental in the energy arena. It has been the one of RES.

with the highest structural modifications in all its 5 With strong development of RES the share of fossil

subsectors, namely power generation, transmis- fuels will decrease in the electricity sector. In 2035

sion, distribution, sales and consumers/clients. power production from fossil fuels will approxima-

This is due to market redesign (often via privati- tely equal that from RES, with wind and solar con-

zations) and technology developments. There are tributing approx. two thirds of the total of RES.

great challenges for its future, considering among Due to rationalizations, technology improvements

others: and new energy efficiency policies, the decoupling

• RES integration and distributed generation between GDP growth and energy/electricity con-

with relevant flexibility requirements at all the sumption growth is increasing. The intensity of CO

2

levels; emissions (t CO per 1000 $ of GDP) will generally

2

• storage systems integration at all levels; decrease, also in China, reaching a projected value

• massive introduction of power electronics and in 2040 in the range 0.75-1.5 for most main eco-

automation; nomies.

• integrated optimum dispatching and control of Over the next 15 years world population grew at a

the power flows from many more generators rate of 0.85% p.a., vs. an increase in primary ener-

to the consumers; gy consumption of 1.2% p.a. and 2% for electricity.

• integration of the expected development of The largest energy and electricity market is Asia

electric vehicles and heat pumps; Pacific, responsible for around 50% of the total,

• building automation, smart meters, demand with China alone at around 25%.

Tendenze mondiali

nella produzione

e consumo di elettricità

L’articolo presenta la situazione attuale della produzione e consumo di elettricità dalle varie

fonti nelle aree del mondo e gli sviluppi avvenuti negli ultimi 15 anni. Vengono riportate le

previsioni relative alla futura penetrazione delle differenti tecnologie e i principali fattori che le

condizionano.

Viene sottolineata la sempre maggior importanza dell’elettricità nel settore energetico; la

pervasiva introduzione delle tecnologie ICT ha aperto la strada a nuovi modelli di business

con la comparsa di nuovi stakeholders.

Impiantistica Italiana - Gennaio- Febbraio 2018 31